Typical liberal last gasp, to call someone a racist when they can't refute what has been said. Thank you Al Sharptounge !Non-existent problem? We're fat as shit, you fucking moron. As for racist, look at this post, or any post you make for that matter. 'Gubmint'?

And her school lunch efforts have wasted lots of taxpayer money on crap that the children WON'T eat and is therefore food is wasted. Typical liberal solution to a non existing problem. And then crow that it's a "success" in the liberal gruberites eyes, that they 'hope and changed" the diet of the children, when the wasted taxpayer dollars in food that's mandated for the school districts to buy, or loose Gub'mint moneys, is throw away when the children DON"T eat it ! Typical of all odummer's failing progroms there comrade Dough Boy ! Originally Posted by Rey Lengua

- WombRaider

- 06-09-2015, 04:13 PM

- Rey Lengua

- 06-09-2015, 04:38 PM

Non-existent problem? We're fat as shit, you fucking moron. As for racist, look at this post, or any post you make for that matter. 'Gubmint'? Originally Posted by WombRaiderIf YOU'RE "fat as shit", why don't you get up off your knees from behind the dumpsters at Talleywackers and go exercise ? On is that how you prefer to burn your calories, by giving back-to-back bare back hummers ? And if the kids are only eating ONE square, nutritious meal a day and not exercising since they're watching the Kardasians and / or not getting enough exercise from chores around the house or playing, then your Queen's attempts to deal with childhood obesity are even more of a joke. But since you and your liberal ilk are a friggen joke, and will NEVER admit that anything the odummers do is wrong, the problem won't go away wit the liberal "lets throw money at it and call it a success" approach ! THE CHILDREN WON'T EAT THE BS SHE'S PUSHING, YA SHITHEAD !!

- WombRaider

- 06-09-2015, 07:11 PM

If YOU'RE "fat as shit", why don't you get up off your knees from behind the dumpsters at Talleywackers and go exercise ? On is that how you prefer to burn your calories, by giving back-to-back bare back hummers ? And if the kids are only eating ONE square, nutritious meal a day and not exercising since they're watching the Kardasians and / or not getting enough exercise from chores around the house or playing, then your Queen's attempts to deal with childhood obesity are even more of a joke. But since you and your liberal ilk are a friggen joke, and will NEVER admit that anything the odummers do is wrong, the problem won't go away wit the liberal "lets throw money at it and call it a success" approach ! THE CHILDREN WON'T EAT THE BS SHE'S PUSHING, YA SHITHEAD !! Originally Posted by Rey LenguaYou'll never admit anything they do is right. Why do you demand something of me that you won't do yourself?

- flghtr65

- 06-14-2015, 02:44 PM

I didn't pay a fine(tax) I got an exemption and I will next year too... It's a ruse, you fucking Ozommunist... Originally Posted by IIFFOFRDBBLOCKHEAD,

I don't care if you get an exemption for the next 30 years. Is it a ruse, when Allstate uses the premiums from low risk drivers to pay of the claims submitted by drivers who total their cars?

ALL Insurance companies make their profit by the exact same way. The premiums from low risk policyholders pay off the claims of the high risk policyholders, you brain dead degenerate repubtard retard. Your guy Mitt had the individual mandate for Romneycare. Is Romneycare a ruse?

- flghtr65

- 06-14-2015, 02:57 PM

Interesting that you didn't reference the escalating price of the "non compliance fee" or that the link I provided said how easy it was to get an exemption from the fee without purchasing insurance or being on Medicaid. Originally Posted by gnadflyGadfly, the amount of the penalty was not the issue that Whirly raised in post #61. The issue for him was the administration calling the penalty a fine and Chief Justice Roberts calling it a tax. Mentioning the year two amount for non compliance was not germane to the issue Whirly raised.

- IIFFOFRDB

- 06-14-2015, 03:23 PM

BLOCKHEAD,

I don't care if you get an exemption for the next 30 years. Is it a ruse, when Allstate uses the premiums from low risk drivers to pay of the claims submitted by drivers who total their cars?

ALL Insurance companies make their profit by the exact same way. The premiums from low risk policyholders pay off the claims of the high risk policyholders, you brain dead degenerate repubtard retard. Your guy Mitt had the individual mandate for Romneycare. Is Romneycare a ruse? Originally Posted by flghtr65

Thanks for the bump!!!

Bad drivers pay higher rates and Massachusetts is a sovereign state... Ozommunist

.

- IIFFOFRDB

- 06-14-2015, 03:33 PM

frightr special...

MATHEMATICS, RATE REVIEW, VISUALIZATIONS

WHY NET PREMIUM INCREASES WILL OFTEN BE EVEN LARGER THAN YOU THINK

JUNE 5, 2015

Ive written before that net premium increases for many individuals purchasing policies under the ACA will be higher than gross premium increases. Ive gotten some emails expressing puzzlement over this conclusion. So, in this post I want to explain in some detail why this is the case.

An example

Consider five Silver policies on an Exchange. In 2015, here is a table showing their gross premiums

1. $4,161.55

2. $3,881.27

3. $4,338.10

4. $4019.11

5. $3550.64

So, the second lowest silver policy is Policy 2, which has a premium of $3,881.27. Suppose our individual can contribute $1,000 per year based on their income. If they had purchased policy 2 their tax credit would have been $2,881.27 and their net premium would have been $1,000. If our individual purchases policy 4, however, which has a gross premium of $4,019.11, their tax credit is still $2,881.27, so they will end up having a net premium of $1,137.84

Now, suppose the gross premium increases average about 6.33% but are distributed as follows among our 5 insurers.

1. 11.38%

2. -2.57%

3. 7.26%

4. 10.28%

5. 5.29%

The new gross premiums for 2016 are thus as follows:

1. $4,634.99

2. $3,781.70

3. $4,652.87

4. $4,432.30

5. $3,738.41

The new second lowest premium is Policy 2, which has a gross premium of $3,781.70. Suppose now our individual has essentially the same income such that the amount they are deemed to be able to contribute is still $1,000. This means the 2016 tax credit is $2,781.70. What if our individual wants to keep his health plan and stick with Policy 4. Maybe our individual likes the practitioners in the Policy 4 network. The new difference between the new gross premium for Policy 4 ($4,432.30) and the tax credit of $2,781.70 is $1,650.60.

Thus, although the gross premium for the policy has gone up 10.28% (bad enough) the net premium has gone up 45.06%.

So, did I concoct some bizarre set of numbers so that the ACA would look bad? I did not. The result you are seeing is baked into the ACA.

An experiment

Lets run the following experiment. Suppose premiums are normally distributed around $4,000 with a standard deviation of $500. And suppose the gross premium increase is uncorrelated with premiums and is normally distributed around 5% with a standard deviation of 5%. Assume there are five policies at issue. We can then calculate for each of the five policies, the gross premium increase and the net premium increase in the same way we did in the example above. We run this experiment 100 times.

The graphic below shows the results. The horizontal x-axis shows the size of the gross premium increase (in fractions, not percent). And the vertical y-axis shows the size of the net premium increase. The dotted line shows scenarios in which the gross premium increase is the same as the net premium increase. What we can see is that for the larger gross premium increases, the net premium increases tends to be larger than the gross premium increases and for the smaller gross premium increases (or for gross premium decreases), the net premium increase tends to be smaller than the gross premium increase. Thus, about half the population will experience net premium increases larger and sometimes way larger than they might think from reading the news.

Is this result an artifact of, say, having our policyholder being deemed by the government to be able to contribute $1,000 based on their income? Not really. The graphic below runs the same experiment but this time assumes our individual is poorer and is thus deemed able to contribute only $500.

What we can see from the graphic is that the result is even more dramatic. The poor will see drastic divergences between gross premium increases and net premium increases. Many, for example who have gross premium increases of say just 5% experience net premium increases of over 30%.

And what of the less subsidized purchasers, those who, for example, are deemed able to contribute $3,000 towards a policy? The graphic below shows the result.

Now we can see that the gross premium increases and net premium increases are clustered pretty tightly together. Indeed, for the wealthier purchasers, net premium increases more often than not are smaller than gross premium increases. However, since most purchasers of Exchange policies tend to be those receiving large subsidies, the graphic above is not representative of the situation for most purchasers.

Did I rig the result by assuming that the income-based contribution stayed the same. No. Heres a graphic showing gross versus net premiums first, under the assumption that income-based contributions remain the same and second, under the assumption that income-based contributions wander, sometimes going up, sometimes going down.

What you can see is there is not much difference between the yellow points income based contribution remains the same and the blue points income based contribution wanders.

And, although I wont lengthen this post with yet more graphics, the basic result generalizes to situations in which there are more than 5 Silver policies. The pattern is the same.

Conclusion

It really is true. Net premium increases will often be larger than gross premium increases, particularly for the poor. The sticker shock some received on seeing the gross premium increase figures recently released at healthcare.gov will, in many instances, be little compared to the knockout blow that will occur when people start computing their new net premiums.

- flghtr65

- 06-14-2015, 03:43 PM

Thanks for the bump!!!In auto insurance bad drivers are high risk and they do pay higher rates, but their higher rate (does not cover the cost of their claim) that is why premiums from low risk drivers are used to cover it. You don't understand a Fucking thing about insurance do you?

Bad drivers pay higher rates and Massachusetts is a sovereign state... Ozommunist

. Originally Posted by IIFFOFRDB

With health insurance people who are older (even if they are healthy) pay a higher rate because they are a higher risk.

Mass may be a sovereign state but they get a check from the federal government to help pay for "Romneycare". You are welcome REPUBTARD RETARD.

- IIFFOFRDB

- 06-14-2015, 03:52 PM

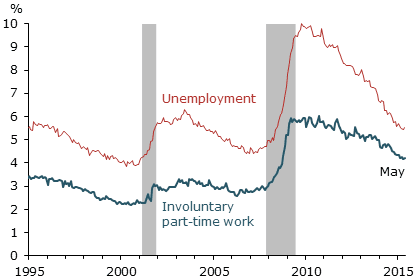

Healthcare Reform, Insurance Costs, Overtime Laws and the Mounting Regulatory State Driving Up Part-Time Work

This is from the Federal Reserve Bank of San Francisco, the bold emphasis is mine. Huh, I wonder what those "long term structural factors" could be?

The incidence of involuntary part-time work surged during the Great Recession and has stayed unusually high during the recovery. This may reflect more labor market slack than is captured by the unemployment rate alone. ...

[T]he ratio of the rate of involuntary part-time work [people who work part time but would prefer to work full time] to the unemployment rate has been rising over time, especially since 2010 but also during the 2002–07 recovery. The ratio rose from about 0.55–0.60 during the late 1990s to about 0.75 in early 2015. This trend increase in the prevalence of involuntary part-time work relative to the unemployment rate suggests that long-term structural factors may be boosting employers’ reliance on part-time work. ...

Involuntary part-time work vs. unemployment

http://benefitrevolution.blogspot.co...nce-costs.html

.

- flghtr65

- 06-15-2015, 08:13 PM

frightr special...ConclusionBlockhead, we already know that rates are going up in the states where the majority of the new policyholders were "already sick". In states where the risk pools have a mix of high risk and low risk people the rates are not going up 40 per cent. FYI, two dimensional graphs are taught in algebra. Go back to school and get your GED so you can understand what you post you repubtard retard.

The sticker shock some received on seeing the gross premium increase figures recently released at healthcare.gov will, in many instances, be little compared to the knockout blow that will occur when people start computing their new net premiums Originally Posted by IIFFOFRDB

- IIFFOFRDB

- 06-15-2015, 08:57 PM

Blockhead, we already know that rates are going up in the states where the majority of the new policyholders were "already sick". In states where the risk pools have a mix of high risk and low risk people the rates are not going up 40 per cent. FYI, two dimensional graphs are taught in algebra. Go back to school and get your GED so you can understand what you post you repubtard retard. Originally Posted by flghtr65

frightr, you're a fool on the stool.

It really is true. Net premium increases will often be larger than gross premium increases, particularly for the poor. The sticker shock some received on seeing the gross premium increase figures recently released at healthcare.gov will, in many instances, be little compared to the knockout blow that will occur when people start computing their new net premiums.

- flghtr65

- 06-15-2015, 09:28 PM

frightr, you're a fool on the stool. Originally Posted by IIFFOFRDBThe two dimensional graphs are only applicable for the states that had large risk pool imbalances. It is not for every state you Fucking IDIOT. The health insurance companies are not asking for steep rate increases in every state. Go back and read post # 1, MORON. Before this law was passed the poor who did not get insurance from their employer had no health insurance at all. There are millions of poor people who are getting the expanded Medicaid. The graphs are only for those who qualified for a private plan and are in certain states that had a large risk pool imbalance.

- IIFFOFRDB

- 06-15-2015, 10:11 PM

- gnadfly

- 06-16-2015, 06:31 AM

.... Before this law was passed the poor who did not get insurance from their employer had no health insurance at all. There are millions of poor people who are getting the expanded Medicaid. The graphs are only for those who qualified for a private plan and are in certain states that had a large risk pool imbalance.[/SIZE] Originally Posted by flghtr65I consider this your surrender post on the Obamacare subject. You finally acquiesce about Obamacare driving up private insurance cost. It's only about "expanded Medicaid." Poor people had "unexpanded Medicaid" already.

- IIFFOFRDB

- 06-16-2015, 07:20 AM

RULE 1 applies for Osoroscare, frightr...

Saul Alinskys 12 Rules for Radicals

Here is the complete list from Alinsky.

* RULE 1: Power is not only what you have, but what the enemy thinks you have. Power is derived from 2 main sources money and people. Have-Nots must build power from flesh and blood. (These are two things of which there is a plentiful supply. Government and corporations always have a difficult time appealing to people, and usually do so almost exclusively with economic arguments.)

* RULE 2: Never go outside the expertise of your people. It results in confusion, fear and retreat. Feeling secure adds to the backbone of anyone. (Organizations under attack wonder why radicals dont address the real issues. This is why. They avoid things with which they have no knowledge.)

* RULE 3: Whenever possible, go outside the expertise of the enemy. Look for ways to increase insecurity, anxiety and uncertainty. (This happens all the time. Watch how many organizations under attack are blind-sided by seemingly irrelevant arguments that they are then forced to address.)

* RULE 4: Make the enemy live up to its own book of rules. If the rule is that every letter gets a reply, send 30,000 letters. You can kill them with this because no one can possibly obey all of their own rules. (This is a serious rule. The besieged entitys very credibility and reputation is at stake, because if activists catch it lying or not living up to its commitments, they can continue to chip away at the damage.)

* RULE 5: Ridicule is mans most potent weapon. There is no defense. Its irrational. Its infuriating. It also works as a key pressure point to force the enemy into concessions. (Pretty crude, rude and mean, huh? They want to create anger and fear.)

* RULE 6: A good tactic is one your people enjoy. Theyll keep doing it without urging and come back to do more. Theyre doing their thing, and will even suggest better ones. (Radical activists, in this sense, are no different that any other human being. We all avoid un-fun activities, and but we revel at and enjoy the ones that work and bring results.)

* RULE 7: A tactic that drags on too long becomes a drag. Dont become old news. (Even radical activists get bored. So to keep them excited and involved, organizers are constantly coming up with new tactics.)

* RULE 8: Keep the pressure on. Never let up. Keep trying new things to keep the opposition off balance. As the opposition masters one approach, hit them from the flank with something new. (Attack, attack, attack from all sides, never giving the reeling organization a chance to rest, regroup, recover and re-strategize.)

* RULE 9: The threat is usually more terrifying than the thing itself. Imagination and ego can dream up many more consequences than any activist. (Perception is reality. Large organizations always prepare a worst-case scenario, something that may be furthest from the activists minds. The upshot is that the organization will expend enormous time and energy, creating in its own collective mind the direst of conclusions. The possibilities can easily poison the mind and result in demoralization.)

* RULE 10: If you push a negative hard enough, it will push through and become a positive. Violence from the other side can win the public to your side because the public sympathizes with the underdog. (Unions used this tactic. Peaceful [albeit loud] demonstrations during the heyday of unions in the early to mid-20th Century incurred managements wrath, often in the form of violence that eventually brought public sympathy to their side.)

* RULE 11: The price of a successful attack is a constructive alternative. Never let the enemy score points because youre caught without a solution to the problem. (Old saw: If youre not part of the solution, youre part of the problem. Activist organizations have an agenda, and their strategy is to hold a place at the table, to be given a forum to wield their power. So, they have to have a compromise solution.)

* RULE 12: Pick the target, freeze it, personalize it, and polarize it. Cut off the support network and isolate the target from sympathy. Go after people and not institutions; people hurt faster than institutions. (This is cruel, but very effective. Direct, personalized criticism and ridicule works.)

Saul Alinskys 12 Rules for Radicals

Here is the complete list from Alinsky.

* RULE 1: Power is not only what you have, but what the enemy thinks you have. Power is derived from 2 main sources money and people. Have-Nots must build power from flesh and blood. (These are two things of which there is a plentiful supply. Government and corporations always have a difficult time appealing to people, and usually do so almost exclusively with economic arguments.)

* RULE 2: Never go outside the expertise of your people. It results in confusion, fear and retreat. Feeling secure adds to the backbone of anyone. (Organizations under attack wonder why radicals dont address the real issues. This is why. They avoid things with which they have no knowledge.)

* RULE 3: Whenever possible, go outside the expertise of the enemy. Look for ways to increase insecurity, anxiety and uncertainty. (This happens all the time. Watch how many organizations under attack are blind-sided by seemingly irrelevant arguments that they are then forced to address.)

* RULE 4: Make the enemy live up to its own book of rules. If the rule is that every letter gets a reply, send 30,000 letters. You can kill them with this because no one can possibly obey all of their own rules. (This is a serious rule. The besieged entitys very credibility and reputation is at stake, because if activists catch it lying or not living up to its commitments, they can continue to chip away at the damage.)

* RULE 5: Ridicule is mans most potent weapon. There is no defense. Its irrational. Its infuriating. It also works as a key pressure point to force the enemy into concessions. (Pretty crude, rude and mean, huh? They want to create anger and fear.)

* RULE 6: A good tactic is one your people enjoy. Theyll keep doing it without urging and come back to do more. Theyre doing their thing, and will even suggest better ones. (Radical activists, in this sense, are no different that any other human being. We all avoid un-fun activities, and but we revel at and enjoy the ones that work and bring results.)

* RULE 7: A tactic that drags on too long becomes a drag. Dont become old news. (Even radical activists get bored. So to keep them excited and involved, organizers are constantly coming up with new tactics.)

* RULE 8: Keep the pressure on. Never let up. Keep trying new things to keep the opposition off balance. As the opposition masters one approach, hit them from the flank with something new. (Attack, attack, attack from all sides, never giving the reeling organization a chance to rest, regroup, recover and re-strategize.)

* RULE 9: The threat is usually more terrifying than the thing itself. Imagination and ego can dream up many more consequences than any activist. (Perception is reality. Large organizations always prepare a worst-case scenario, something that may be furthest from the activists minds. The upshot is that the organization will expend enormous time and energy, creating in its own collective mind the direst of conclusions. The possibilities can easily poison the mind and result in demoralization.)

* RULE 10: If you push a negative hard enough, it will push through and become a positive. Violence from the other side can win the public to your side because the public sympathizes with the underdog. (Unions used this tactic. Peaceful [albeit loud] demonstrations during the heyday of unions in the early to mid-20th Century incurred managements wrath, often in the form of violence that eventually brought public sympathy to their side.)

* RULE 11: The price of a successful attack is a constructive alternative. Never let the enemy score points because youre caught without a solution to the problem. (Old saw: If youre not part of the solution, youre part of the problem. Activist organizations have an agenda, and their strategy is to hold a place at the table, to be given a forum to wield their power. So, they have to have a compromise solution.)

* RULE 12: Pick the target, freeze it, personalize it, and polarize it. Cut off the support network and isolate the target from sympathy. Go after people and not institutions; people hurt faster than institutions. (This is cruel, but very effective. Direct, personalized criticism and ridicule works.)